Executive Summary

Most people can close their eyes and imagine a parent offering this nugget of advice unsolicited: “Paying for rent is throwing your money away.”

Yet, for many small business owners, leasing space can seem like the only move to make. It is true that leasing offers flexibility, fixed monthly costs, and minimal upfront capital. However, over time, those monthly rent checks business owners sign build equity for someone else, not for the business itself.

Looking at the bigger picture, owner-occupied commercial real estate loans are a strong alternative and a tremendous opportunity. Purchasing property where the owner operates builds long-term equity for the business while also stabilizing operating costs and giving the owner greater control over the future growth of the business. “Future” and “growth” are two words not often associated with the word “lease.”

Even with future in mind, not enough business owners are taking advantage of the long-term promise of property ownership. A portion may not think it is within their reach, while others don’t know which lenders to trust or more importantly – they are unaware of what those lenders look for in an applicant.

This guide is essential reading -- and a practical look at what business owners need to know before applying for commercial real estate financing to move through the process with confidence and increase the chances of success.

The Hidden Barrier: Why Commercial Real Estate Loans Remain Elusive for Many Small Businesses

It’s lack of preparation, not access to financing, which is the biggest roadblock many small business owners run into when trying to secure a loan.

According to data from the Federal Reserve Bank Small Business Credit Survey, only about 42% of small businesses applying for financing receive full approval. Most applicants are denied or do not secure the full amount they need. And while credit unions and community-based lenders often show stronger percentages of approvals, denial rates are still consistently high across lending institutions.

Business viability is not the only reason lenders say no. Many businesses are rejected because they are not adequately prepared for how lenders evaluate risk.

Where Applications Fall Short

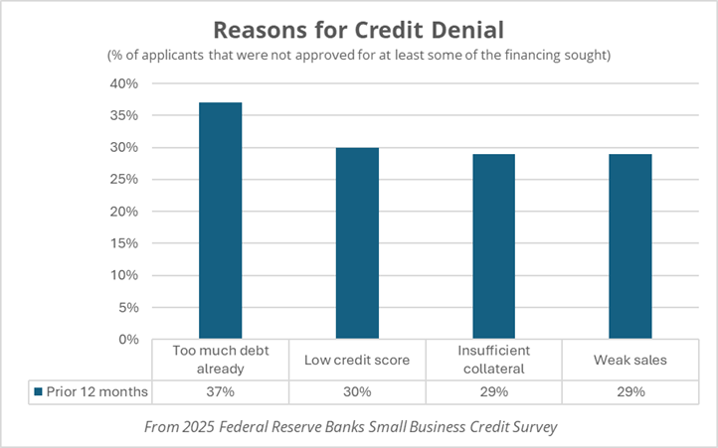

The reasons behind most loan denials are not only common, but they are also usually preventable.

A look at data from the Federal Reserve Bank shows cash flow challenges and credit score profiles near the top of the list of reasons for denial:

In addition, businesses can further hurt their odds with gaps in documentation and misalignment with underwriting expectations. Or in short, they are applying for financing before they are ready to apply for financing.

The Cost of Being Unprepared

It can be tough to pass a test you haven’t studied for. However, not fully understanding a lender’s expectations can have consequences beyond just failing to secure a loan.

- Applications may be delayed or rejected

- Businesses may receive less favorable terms

- Opportunities to secure ideal properties may be lost

- Borrowers may take on loans they are not well positioned to pay back

That last bullet is a risk facing even approved applicants, who can face repayment troubles over the long-term if they enter the lending process unprepared.

The biggest barrier to securing a commercial real estate loan isn’t always access to capital. It’s understanding what lenders need before you apply.” – Betsy Dillingham, Business Lending Director, Addition Financial Credit Union]

Small business owners who understand how lenders evaluate applications, and walk in prepared, are significantly more likely to:

- Secure approval

- Receive stronger terms

- Move forward with confidence

Nowhere is this more important than in fast-growing and fast-moving markets like Central Florida, where being ready to move on a property at the right time can be a catalyst for success.

The Shift: Why More Central Florida Businesses Are Considering Ownership

It is well established by research provided by groups such as Orlando Economic Partnership: Central Florida is still one of the fastest growing areas in the country.

With more than 1,500 new residents moving into the region each week, this sustained growth is fueling demand for a limited supply of real estate across all sectors, from healthcare and hospitality to construction and professional services.

Meanwhile:

- Lease rates are still fluctuating

- Competition for space is increasing

- Long-term occupancy costs become less predictable

These factors prompt a shift in strategy by forward-thinking business owners – from leasing space to owning it.

“For many business owners, the shift from leasing to ownership is not just a real estate decision. It is a long-term financial strategy.” – Miriam Mitchell, Chief Lending Officer, Addition Financial Credit Union

What is an Owner-Occupied Commercial Real Estate Loan?

In the simplest terms, an owner-occupied commercial real estate loan is used to purchase property where the business owner occupies a majority of the space, typically at least 51%.

These loans are commonly used for:

- Office buildings

- Medical or professional spaces

- Retail storefronts

- Warehouses or light industrial facilities

The typical characteristics of an owner-occupied commercial real estate loan include:

- Loan terms of 5 to 20 years

- Down payments generally ranging from 10% to 30%

- Fixed or variable interest rates

Why Credit Unions Are a Strong Option for Small Business Lending

The choice of lending partner can be as significant a decision as the terms of the loan itself.

Even aside from the competitive rates and terms they can offer, credit unions offer a distinct community-focused approach to commercial lending that can be invaluable for small businesses planning for the future.

Relationship-Based Lending: Credit unions focus on long-term relationships, allowing for a deeper understanding of a business beyond just financial statements.

Local Market Insight: Community-based institutions understand the nuances of markets like Metro Orlando -- providing context that national lenders may lack.

Personalized Guidance: From early conversations through closing, credit unions often provide more direct support to help business owners navigate the process.

Member-First Approach: As not-for-profit institutions, credit unions are built to serve their members, often resulting in a more collaborative and supportive lending experience.

One more benefit you might not be aware of: Credit unions are exempt from intangible taxes, and that means the borrower doesn’t have to pay it.

The Takeaway: Top 5 Things Small Business Owners Should Know Before Applying

Below are five of the most crucial factors, according to lending experts, that every business owner, small or large, should keep top of mind before pursuing an owner-occupied commercial real estate loan.

- Cash flow matters more than revenue.

- Know the Debt Service Coverage Ratio (DSCR).

- Preparation, presentation, and documentation can make or break an application.

- Personal credit still plays a key role.

- The right lending partner can improve the chances of getting approved

Looking back at the Federal Reserve Bank survey, insufficient cash flow is one the leading reasons small business loan applications are denied.

While it is great to point to strong revenue on a financial statement, lenders pay closer attention to cash flow, the actual income available to cover loan payments.

Lenders will evaluate:

- Net operating income

- Expense consistency

- Stability of earnings over time

- Liquidity, solvency, and profitability

What this means: A growing business with inconsistent profitability might have a tougher time securing loan approval than a smaller, stable business with steady net income.

Not to bog anyone down with too many acronyms, one of the more critical, and overlooked, metrics is the Debt Service Coverage Ratio (DSCR).

DSCR measures a business’s ability to repay a loan using business income.

A typical benchmark is a DSCR of 1.25 or higher. This means a business generates at least 25% more income than needed to cover loan payments.

Understanding DSCR

|

Scenario |

Outcome |

|

DSCR Below 1.0 |

Not enough income to cover debt |

|

DSCR = 1.0 |

Break-even |

|

DSCR = 1.25+ |

Preferred by lenders |

What this means: Business owners need to calculate the DSCR before applying, or work with

a relationship-based lender who can help you estimate it.

A strong application isn’t built when a business applies. It was built in the months leading up to it.

Underwriters from the smallest of community-based lenders to the biggest of banks can point to scores of examples of having to delay or deny business lending applications simply because their documentation is incomplete or simply disorganized.

Lenders typically require:

- 2 to 3 years of business tax returns

- Profit and loss statements

- Balance sheets

- 2 to 3 years of personal tax returns

- Personal financial statements

- Bank statements

A business with its I’s dotted and T’s crossed will move through the process much faster and with less complications than those who appear to be cramming for a test.

While business owners prepare those all-important documents, they should know – their personal credit profile is still a key factor.

The Federal Reserve Bank survey data shows lenders often rely on personal credit history when making decisions on small business applications.

Why this matters:

- Most loans require personal guarantees

- Credit history is an indicator for financial responsibility

- Strong credit can improve loan terms

What this means: Business owners should review their credit, and address any issues in advance, as well as avoid taking on any new debt before applying.

Here is a sobering truth many small business owners have learned the hard way: A portion of bigger banks will not even loan to smaller businesses.

Besides the fact they are local and see the value in community investment, relationship-focused lenders – such as credit unions – can provide tangible advantages for small business borrowers:

- Offer early guidance before applying

- Help identify gaps in financial documents

- Provide clear explanations of loan structure and expectations

- Ongoing support throughout the process and beyond

Research from the Federal Reserve Bank and the National Federation of Independent Business shows that small businesses often rely on established financial relationships when seeking financing.

What this means: Engaging a lender early who will take the time to work with the business owner can help them avoid surprises and position an application for success.

Case Example: An Aesthetic Salon’s Growth Journey from Leasing to Ownership

To paint the full picture of how preparation and financing go hand in hand, let’s walk through the borrowing process with a hypothetical Central Florida business owner.

The Scenario

Meet Maria: Maria owns a growing aesthetics salon in the SoDo area of Orlando, specializing in skincare treatments and cosmetic services. She has been in business for five years and has steady revenue and a loyal client base.

Currently, Maria is leasing a 1,500-square-foot space in a high-traffic retail center.

- Monthly rent: $8,200

- Lease subject to annual increases

- Limited ability to customize or expand

Maria is getting advice from colleagues, friends, and other business owners that she should consider purchasing her own space as her business grows.

The Opportunity

Maria finds a 2,500-square-foot property that would allow her to:

- Add treatment rooms

- Expand service offerings

- Create a more customized client experience

Purchase price: $1.6 million

The price tag initially makes Maria hesitate – but after speaking to a lender at a nearby credit union and getting a full look at the numbers, she realizes the monthly loan payment could be comparable to her current rent.

The Preparation Phase

Before applying, Maria takes several important steps:

The Outcome

Since Maria came into the process prepared and worked with a lender whom she built a relationship with:

✅Her application moves smoothly through underwriting

✅She secures financing with manageable terms

✅Her monthly occupancy cost becomes predictable

✅She begins building equity in the property

Over time, the property becomes one of her business’s most valuable assets and creates opportunities to explore a second location in the future.

Preparation is the Difference Between Opportunity and Outcome

There are a lot of decisions for small business owners as they plan for the future, and purchasing commercial property can be one of the most impactful.

But securing a loan begins with preparation.

Understanding how lenders evaluate risk, organizing financial documents, and working with the right lending partner can dramatically improve your chances of approval – and the terms and rates of the financing you receive.

That preparation can make the difference in capitalizing on a perfect opportunity in a growing and competitive market like Central Florida.

Ready to Take the Next Step?

Learn how Addition Financial can help your business prepare for and secure owner-occupied commercial real estate financing -- with person-to-person guidance every step of the way.

Fixed rates as low as 5.25% are the lowest in the state of Florida!

https://pages.additionfi.com/spacetogrow

References/Sources

2026 Report on Employer Firms: Findings from the 2025 Small Business Credit Survey

https://www.fedsmallbusiness.org/categories/employer-firms/2026-report-on-employer-firms

Wall Street Journal (Buy Side – Commercial Real Estate Loans Guide)

https://www.wsj.com/buyside/personal-finance/business-loans/commercial-real-estate-loans

National Federation of Independent Business

https://www.nfib.com

National Association of Realtors

https://www.nar.realtor

Orlando Economic Partnership

https://orlando.org

U.S. Census Bureau

https://www.census.gov

Posted on Jun 12, 2026

Topics: